Offshore Wind Installation Forecast Report

Learn about the sector’s key trends, challenges, and opportunities, with a particular focus on vessel supply and demand dynamics. It is focused on the global bottom-fixed offshore wind installation market outside of China.

The complete forecast report is available only to our customers. Get a sample and a free product tour by filling the contact form.

This 45-page report covers

Developer Demand a

- Growth projections

- Market trends and emerging regions

- Trends in turbine and foundation sizes

- Impact of delays on overall market projections

- Recent policy changes and their implications

- Causes of delays, including supply chain issues and regulatory hurdles

Heavy Lift Vessels

- Current supply and future demand

- Fleet segmentation and utilization rates

- Impact of larger turbines and heavier foundations

- Vessel requirements for installation and O&M

- Vessel installation performance

- Increasing maintenance needs and resource allocation

- Downtime due to weather and its impact on project timelines

Cable Laying Operations

- Current state and future needs for cable lay vessels

- Challenges in meeting the growing demand for cable installations

Key takeaways

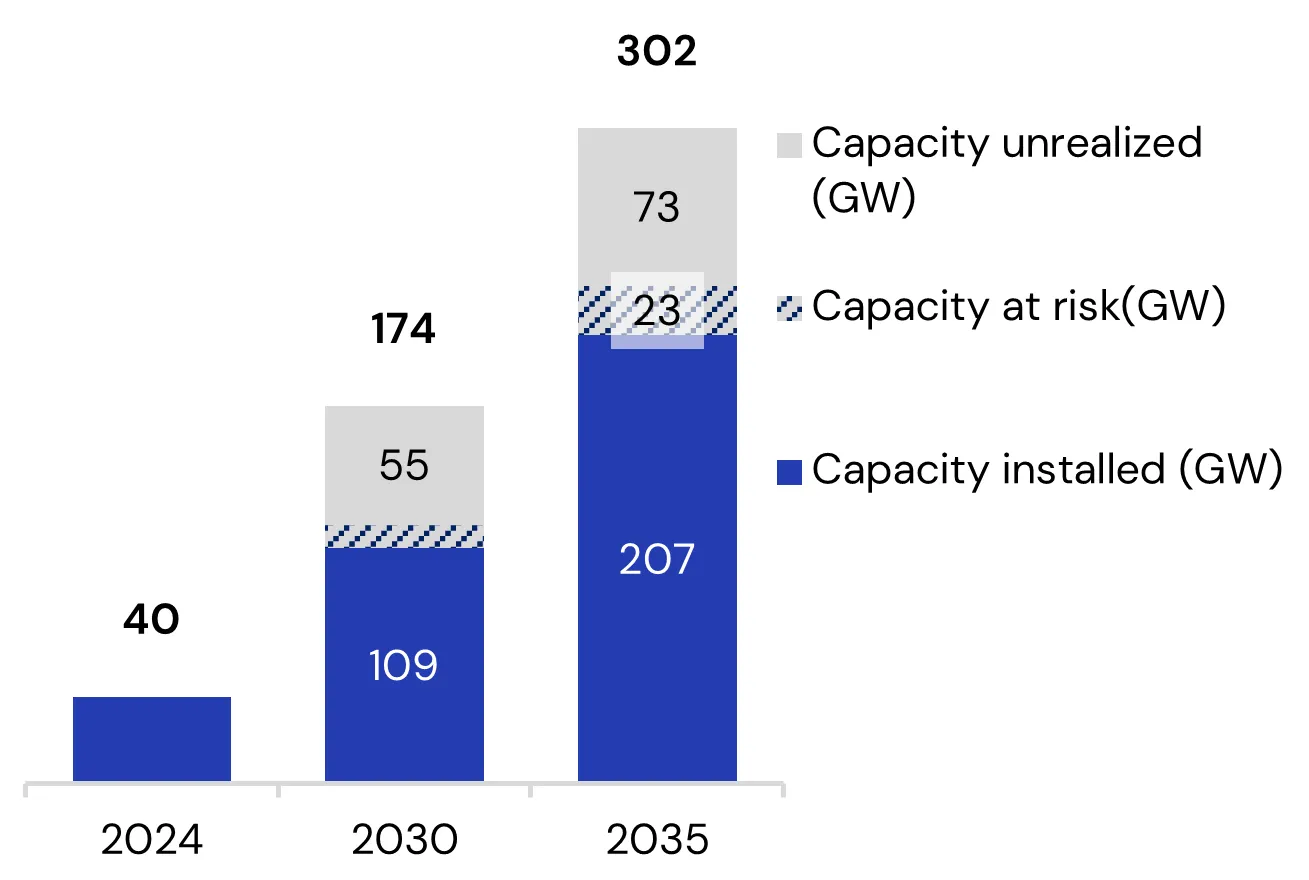

109 GW to be installed by 2030, just two-thirds of the planned capacity

By 2030, from a 174 GW pipeline, 109 GW will likely be installed, potentially reaching 120 GW with a stronger vessel supply and leaving out 55 GW that will not find installation vessels under the current outlook.

By 2035, installed capacity is expected to hit 207 GW, or 68% of the announced bottom-fixed pipeline, reflecting a significant but challenging expansion in offshore wind farms.

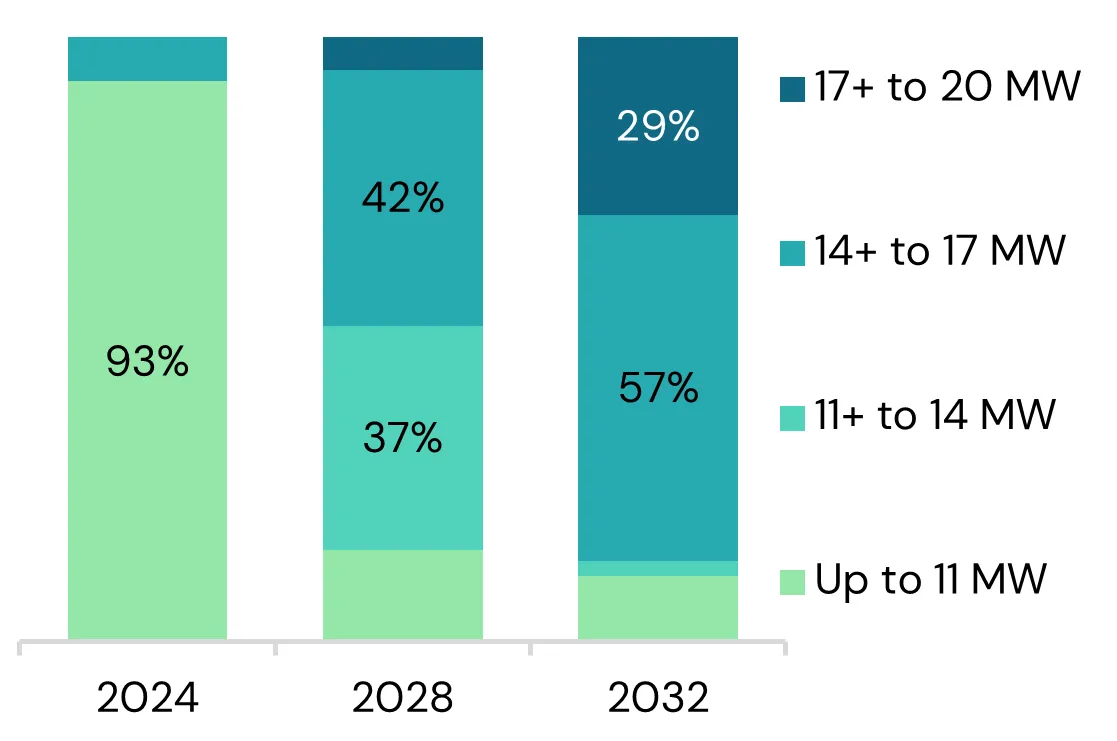

Bigger turbines are coming, despite uncertainty

The 15 MW turbine segment is set to dominate the offshore wind market later this decade, as smaller turbines (11 MW and below) experience a generational fadeout.

The wind turbine industry faces pressures, with soaring costs and geopolitical uncertainty, with China's emerging role through its development of 16 to 22 MW turbines. Despite challenges, developers are driving a shift towards larger turbines.

Heavy-lift vessel demand is over-concentrated around 2030

Too many projects have set construction dates at the end of this decade. Annual heavy lift vessel demand will peak at 75 years' worth of time, overstretching installation fleets.

Heavy component replacements remain time-intensive, with significant increases in vessel demand expected, and maintenance becoming half of all heavy-lift demand.

Interested in getting the report?

Fill in the form to discuss access to the complete forecast report.

Frequently Asked Questions

You have questions. We have answers.

How often will the report be updated?

The report will be updated twice a year, with the next update scheduled for Q1 2025. A public webinar will be held in Q4 2024

What if I have additional questions?

You are welcome to discuss the forecast in detail with us. For any questions, please email us at insights@spinergie.com.