Hélia Briaud

,

Subsea Cable Analyst

Author

, Published on

March 23, 2026

No items found.

How rising cable repair demand is impacting how contracts are structured and what the market can expect by the mid-2030s.

.webp)

Cable failures can occur for a variety of reasons. As with any industrial component, manufacturing defects, improper handling, installation issues, or fatigue can all play a role. However, the root cause will often depend on the type of cable.

Cable aging, environmental stresses, design challenges, and the scaling-up of technologies can all contribute to an increase in cable failures.

The trend towards larger wind farms presents distinct challenges for both wind export and array cables. This trend means that export cables are becoming longer and more exposed which increases their vulnerability to environmental and operational risks. For export cables and interconnectors, an additional risk factor comes from their routing through busy maritime zones. Since 2016, many failures have been recorded at depths accessible to vessel anchors—an average of around 50 metres is the most common failure depth, which is well within the range of anchoring activities.

Meanwhile, array cables need more sections due to a larger number of turbines. This leads to a higher number of connection points—which are often critical failure spots.

Cable failures impact cable operators—whether offshore wind farm developers, transmission system operators (TSOs), or public and private interconnector operators—both operationally and strategically.

Operationally, cable failures lead to a halt in energy transmission, causing loss of revenue and additional costs. For example, during the 2020 Malta-Sicily interconnector failure, Enemalta’s contingency plan required running all available power plants, which incurred expenses around €150,000 per day. Moreover, repair works are often constrained by the limited availability of specialized vessels which extend downtime and further complicate logistics.

Strategically, the industry is seeing a shift in how cable contracts are structured. Increasingly, EPCI contracts now include long-term O&M services, requiring companies to adapt to this expanded scope. These contracts can take the form of project-based agreements or extended partnerships. Notably, in spring 2025, DeepOcean secured a four-year framework agreement for O&M services with Vattenfall, while N-Sea signed a seven-year framework with global cable solutions provider Prysmian to handle maintenance and repairs. This evolution highlights the growing importance of integrated solutions combining installation and lifecycle management to better address cable failures and maintenance needs.

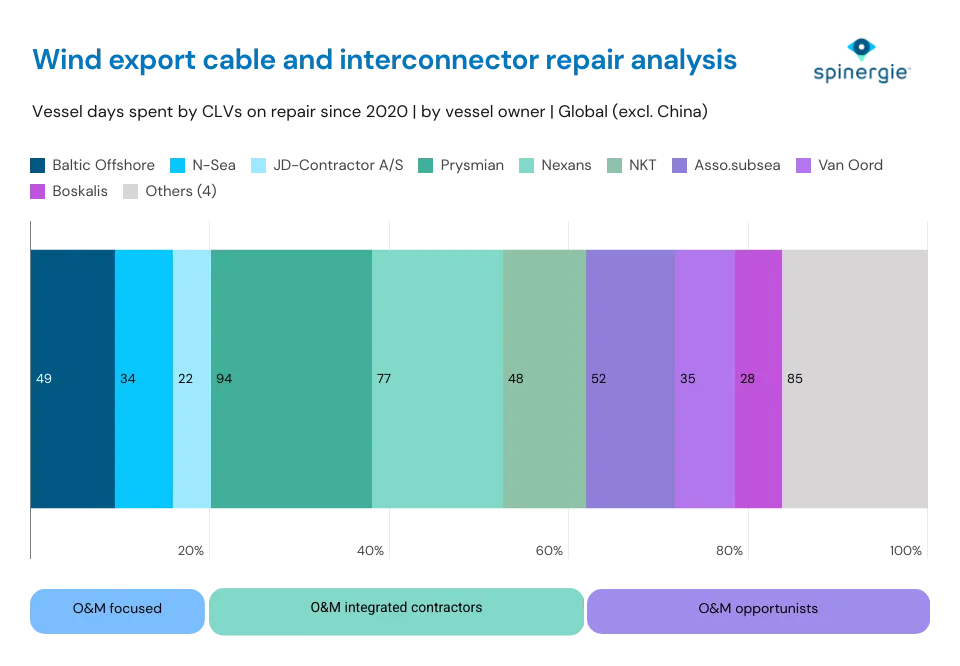

The cable layer vessel (CLV) owners that undertake repair operations can be divided into three categories:

For now, the cable repair market is dominated by opportunistic players and EPCI contractors with each accounting for about 40% of CLV vessel days spent on repairs since 2020. The share of O&M opportunists like Boskalis or Asso.subsea is significant as the sector remains relatively unstructured.

EPCI contractors such as Prysmian and Nexans, are expected to see their share increase because, according to DNV, 80% of offshore wind insurance claims are linked to subsea cable failures. This is pushing developers to demand EPCI contracts that also cover O&M. The CLVs operated by these two categories of players are often best suited to complex deepwater repairs thanks to their capabilities and well-trained crews.

However, there is increasing demand for these CLVs in the installation market. With a number of vessels already committed to large-scale projects, there is growing pressure to develop dedicated repair-focused assets to ensure timely maintenance and reduce operational bottlenecks.

A smaller but growing share of the market is covered by vessel owners with a strong focus on O&M, such as Baltic Offshore, JD Contractor, and N-Sea, who concentrate largely on repair activities. Baltic Offshore and JD Contractor typically operate older CLVs, some around fifty years old, which have become obsolete for large-scale cable installations but have been repurposed for repair work.

A clear sign of market evolution is N-Sea’s announcement of a new CLV dedicated exclusively to repairs: the Altera, expected in 2026, featuring a 4,500-ton carousel capacity. This newbuild marks a major advancement toward specialized vessels designed to meet the growing demands of the repair market.

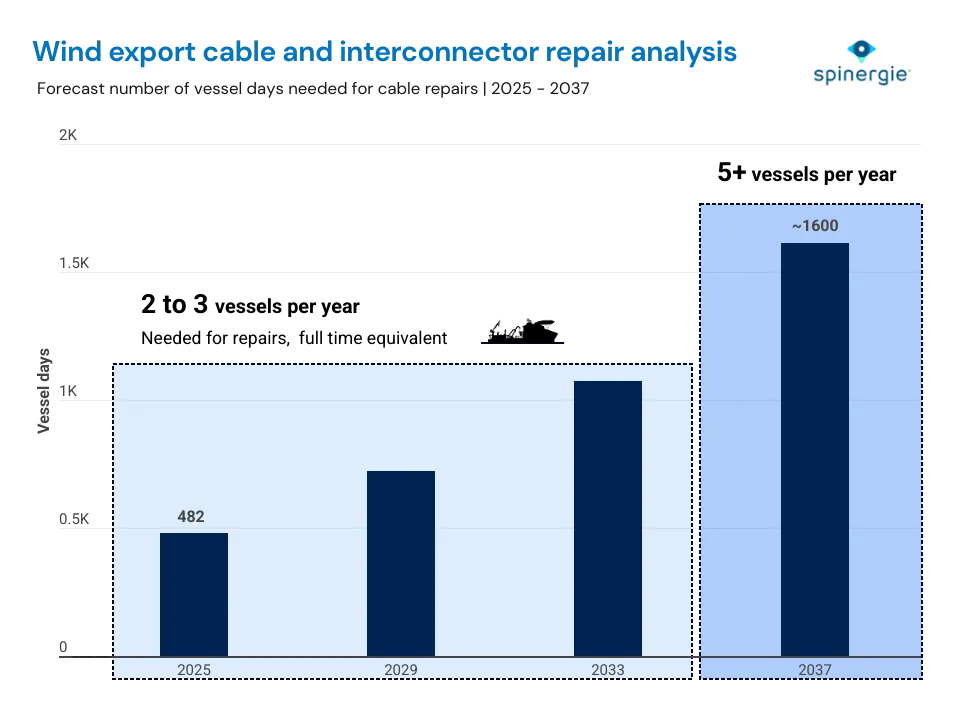

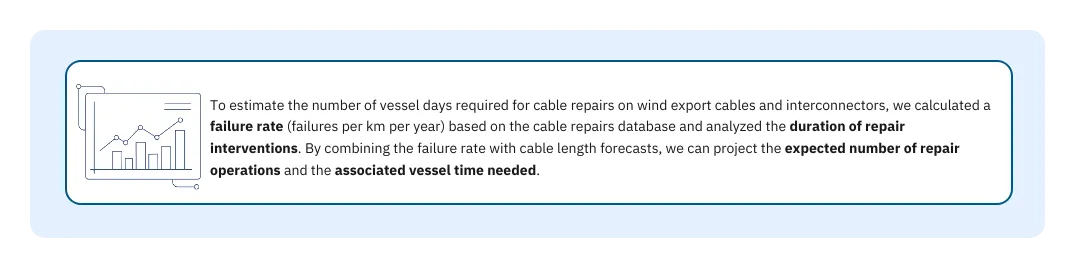

Spinergie forecasting shows that O&M vessel demand (in vessel days) will more than triple between 2025 and 2037—rising from today’s equivalent of two full-time vessels to around five by 2037. This surge reflects the rapid expansion of active subsea cable networks — from 39,000 km in 2025 to 146,000 km by 2035 for wind export cables and interconnectors.

As demand rises, pressure on available repair vessels is likely to intensify, particularly if CLVs remain the primary choice for these operations. CLVs are often selected for their carousels, deck equipment, and experienced crews, and between 2022 and 2024, they represented 43% of vessel days dedicated to export cable repairs.

Diversifying the types of vessels used could help address this growing need. When CLVs are not available, or when repairs are less complex, construction and multipurpose vessels are also deployed. Equipping these vessels with more suitable technology may help balance fleet capacity and cost management. This approach is reflected in recent contracts—in April 2025, DeepOcean announced a four-year framework agreement with Vattenfall for cable maintenance activities.

Spinergie’s Cable Repairs Database page offers a customized experience for Cable Module subscribers, consolidating all of our offshore wind power cable repairs data (export, interconnectors and array).

The database gives full access to detailed information on failures, vessel activities, and repair timelines. From the consolidated list of past repair campaigns, key metrics can be analyzed, including failure rates across various factors (such as water depth and cable specifications), repair lead times or average repair durations.

Find out more about how the Cable Repairs Database can help in your project planning, request a free demo and discussion today: book a demo.