Hugo Madeline

,

Senior Offshore Energy Analyst / Project Manager

Author

, Published on

March 23, 2026

No items found.

The offshore vessel sector is responding to a cooling oil and gas market. Senior offshore energy analyst Hugo Madeline explores this impact with the key trends and sector dynamics.

.jpg)

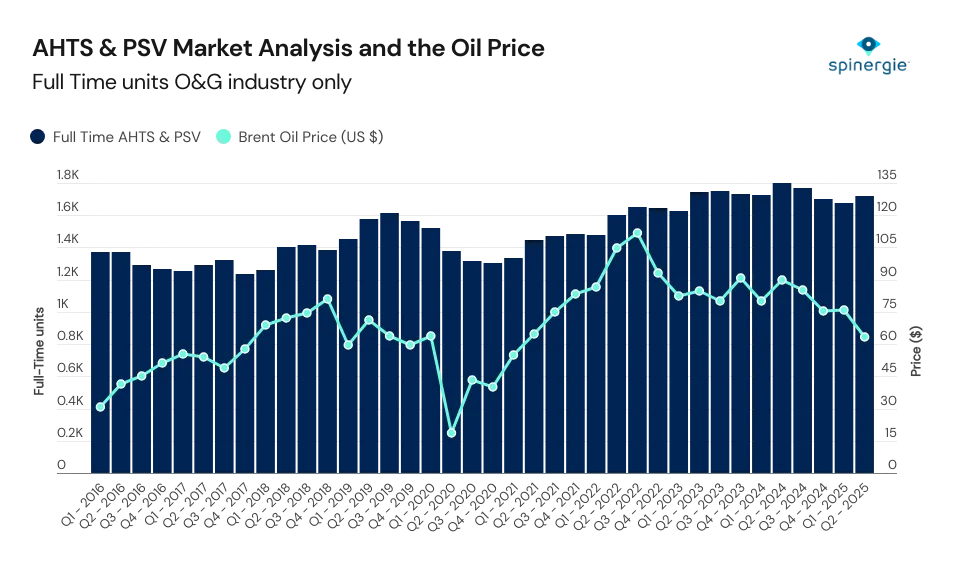

After a growth period through 2023 and 2024, the oil and gas (O&G) market has begun to slow. Inevitably, being closely tied to offshore rig activity and the oil price, the Offshore Service Vessel (OSV) sector faces a similar shift.

While Spinergie data indicates that there was a slight uptick in activity during the second quarter of 2025 some key questions remain: How will the OSV market—here meaning Anchor Handling Tug Supply (AHTS) and Platform Supply Vessel (PSV)—respond to that uptick? Should we expect stabilization or a decline in activity? What market drivers should we watch?

Understanding the dynamics behind each of these questions is the best way to anticipate the next phase.

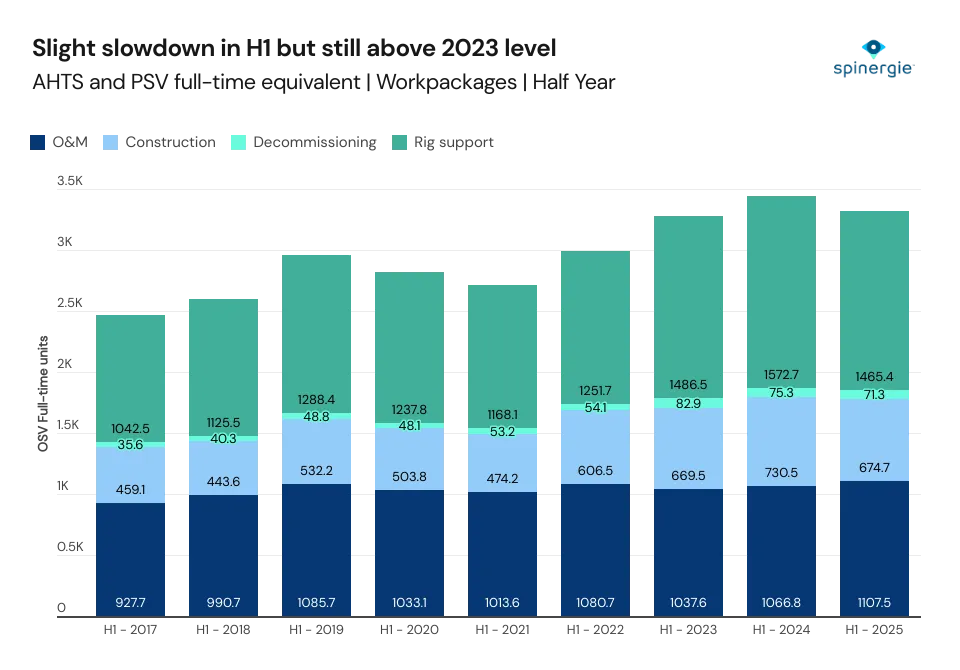

Data gathered by Spinergie shows that there has been an overall increase in the total number of OSV units between 2017 and 2025. Rig support vessels showed notable growth between 2021 and the peak of 2024, however, it has since begun to decrease. This follows the contracted rig rate which also peaked in 2024.

Operations and Maintenance (O&M) has remained steady, however, the current-half year trend shows an inversion. While there is stability in the O&M sector, both the construction and rig support sectors show decline in H1 2025 compared to last year. This combination of factors has brought the activity level back to around 1H 2023 levels.

A further slowdown factor centres around the O&G market. In the post-Covid years, many of the postponed exploration and field development projects were finally able to begin. However, investments are not increasing and the number of new Final Investment Decisions (FIDs) remains flat year after year.

Growth will remain limited until new developments increase. Similarly, as the contracted rig count falls, support activities follow.

Overall, the health of the global OSV sector is highly dependent on the rig market, which has begun to show signs of a slowdown.

The number of FPSO installations are expected to decline in 2026 following a 2025 peak from Covid-postponed projects. As the pandemic caused a drop in new investments, and FPSOs take three to four years to build, there will be an impact on installation activities during this mid-2020s period.

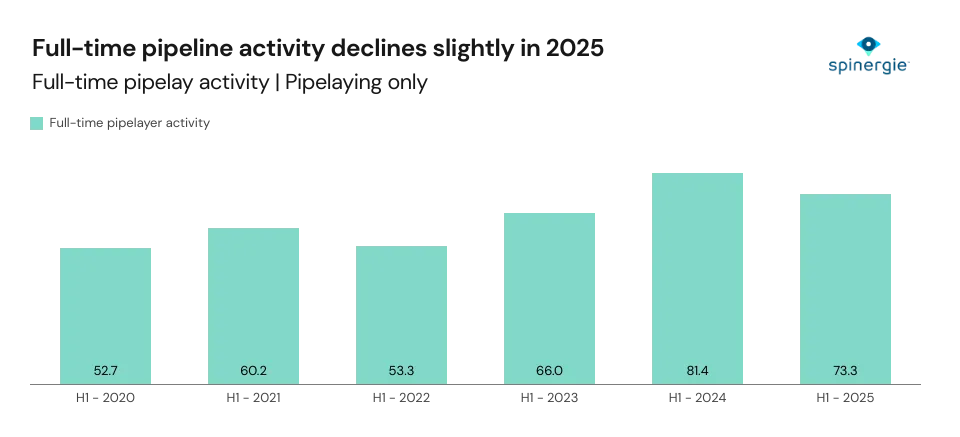

Pipelay activity has decreased from 2024 levels in the first half of 2025. However, it is still above 2023 levels. The market can expect to see sustained interest in this sector which will lead to increased OSV activity.

We expect pipelay to follow the same trend as FPSO installation and likely see a decline in 2026.

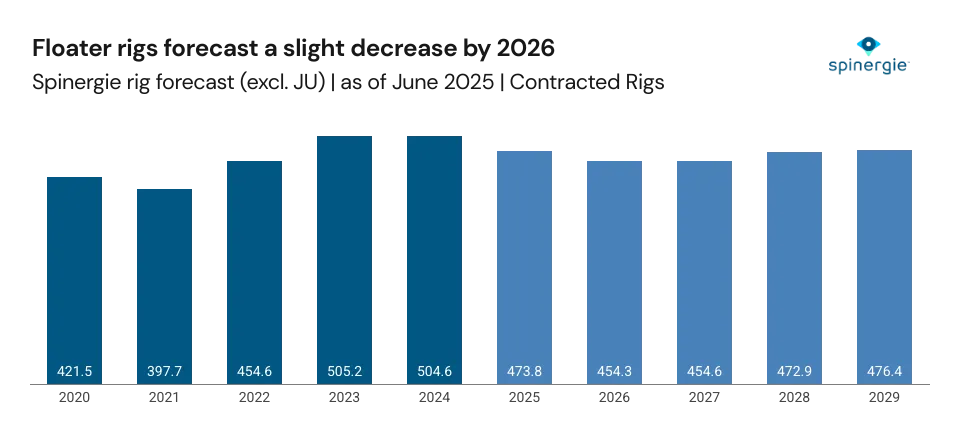

Due to lack of O&G investments, the floater rig market is in slight decline. Spinergie data indicates that floater activity will bottom out around 2026 to 2027 followed by stabilization. We do not expect this to affect OSVs in 2025. Instead, construction activity will drive the OSV sector, not rig support.

Decreased future demand is expected to place downward pressure on dayrates.

This is a pivotal year in the OSV sector. While short-term construction activity may support sustained AHTS and PSV demand, there are broader signals of a slowdown including a reduced need for rig support, flat FID rates and a forecasted dip in FPSO installations.

Whether this can be classed as stabilizing or slowing down depends on future offshore investments. There remains some cautious optimism but the long-term health of the OSV sector remains tied to that of upstream oil and gas.