Jean-Baptiste Rougeot

,

Head of Analysts

Author

, Published on

March 23, 2026

Sarah McLean

,

Lead Content Manager

Co-Author

What are the key trends and opportunities shaping the OSV sector and what comes next for the largest and most diverse offshore fleet?

.webp)

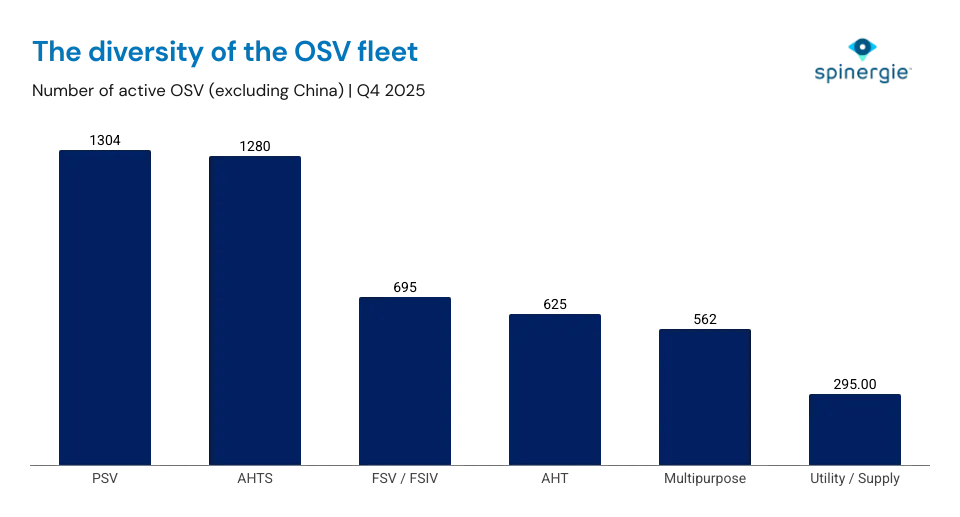

Offshore Supply (sometimes service) Vessels—OSVs—make up 43% of the global offshore fleet: the largest vessel fleet in the sector. The almost 4,800 vessels comprise multiple types with varied roles from supply, crewing, refuelling, towing, and light construction.

While some definitions vary, Spinergie classifies the following as the main OSV vessel types:

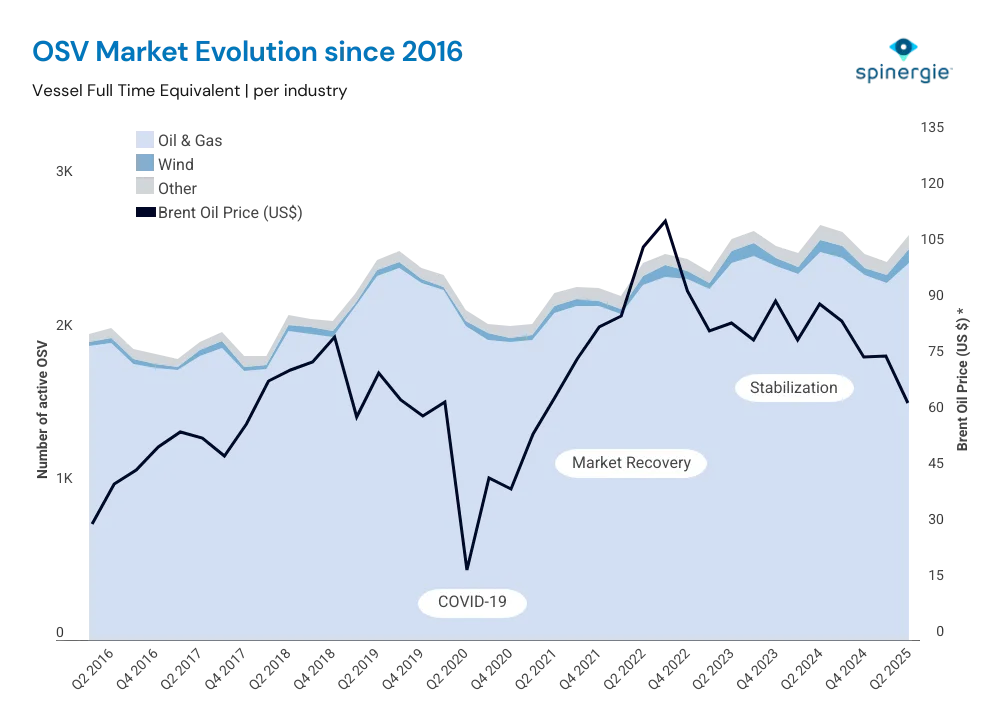

Five years ago, the COVID-19 pandemic caused an OSV demand crash made all the more impactful because of the peak witnessed in 2019. After the difficulties of 2020, recovery began in earnest during 2021 and reached the 2019 record in 2023. Growth continued into 2024, but in the third quarter of that year, the sector once again saw some tension and a decline in demand.

The main reason behind this decline is that the market simply “caught up” with the backlog caused by the COVID-19 downturn. In the initial flurry of activity, and as projects resumed, demand rose quickly alongside dayrates and utilization. Vessel owners also undertook strategy shifts in order to become profitable again and the OSV sector entered a consolidation phase.

Other notable factors include:

This market stabilization has resulted in less favourable conditions for new offshore developments and increased cash and cost management discipline from offshore developers and operators.

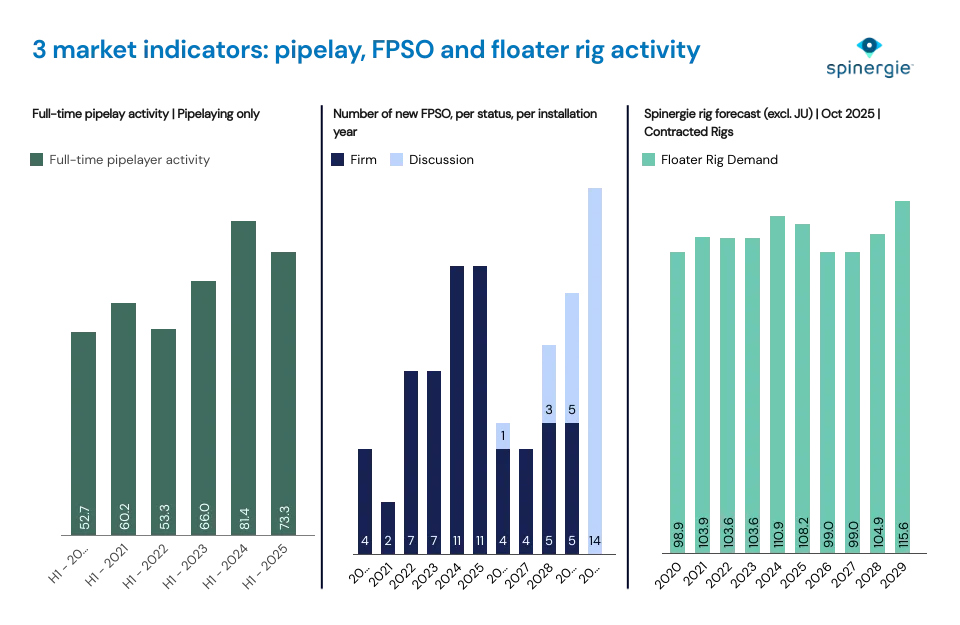

There are three key indicators that can be used to predict when OSV demand will move from stabilization to growth: the offshore rig market, construction activities, and FPSO installations.

OSVs correlate closely with offshore rig activities which account for 22% of the OSV fleet’s supporting operations. Generally, offshore rig trends see OSVs follow a similar trajectory approximately a year later. So, as we currently expect the offshore rig market, particularly deepwater, to pick up again in 2026, it is reasonable to assume the OSV sector will follow suit in 2027.

Pipelay vessel activities are a good marker of offshore construction activities. There was a lack of new investment during COVID, which is now having an impact on today’s activities. Furthermore, construction activity was slow to pick-up post COVID (peaking in 2024). We currently anticipate stabilization will continue in offshore construction until late 2026—once again indicating OSV would follow around 2027.

The final marker will be the number of installed FPSOs. Indeed, this is perhaps the strongest indicator as the lead-times involved in building or converting FPSOs makes them easy to track and identify market indicators. Here we have observed the same trends as pipelay and offshore rigs. The 2024 peak corresponds with the project delays of 2021. A downturn is anticipated in 2026, representing a lack of new investment between 2022 and 2024, yet activity is clearly increasing from 2027.

The OSV fleet is notable for its resilience. Today, most of the peaks and falls of demand are absorbed by the laid-up fleet by laying-up or reactivating according to market needs. This laid-up fleet allows for rapid increases or decreases in vessel count and directly impacts the utilization rate by 5-10%.

However, the laid-up fleet is aging and vessels over 15 years old are unlikely to be reactivated due to the prohibitive costs involved. This means that, with market recovery expected in approximately two years, fleet age becomes increasingly relevant. There are two solutions: retrofitting the incumbent fleet and engaging in a newbuild program. Given the current tight state of the market, newbuild investment is especially complex.

Within the wider global outlook, there are regional variations to take into account. Here we identify the main points for the key global OSV markets, but for a more in-depth analysis please refer to our recent webinar: ‘OSV Demand Outlook: Identifying the next growth drivers’.

The Middle East OSV market is characterized by a large appetite for smaller AHTS and PSV. Despite Saudi Aramco reducing its rig count, OSV activity has not yet decreased. This is because the fleet remains engaged in construction activities—which remains high—and towing off-contract jackups to other regions or for stacking. A slight slowdown is anticipated but overall, the Middle East OSV fleet is expected to remain constant.

Africa is poised to play a significant role in future OSV activities. Nigeria’s resumption of activity is expected to be a major growth area while there are promising signs from Cote d’Ivoire, Namibia and Mozambique. However, Angola’s future activity looks likely to remain muted as oil production has not resumed to previous levels and the shift to gas is slow.

As is often the case in this region, turning O&G exploration into firm development projects, is a major challenge.

In the U.S. Gulf of Mexico, OSV demand reflects shifting offshore strategies. Fast tie-back projects now dominate. This means there is steady vessel demand as operators use existing infrastructure to develop new finds quickly and cheaply. In contrast, large deepwater greenfield projects are rarer, but require up to 10 times higher OSV demand when they occur. In all, this creates a market of consistent low-level activity punctuated by demand spikes. Now, with offshore wind paused, OSV is expected to find additional growth through decommissioning activities.

The North Sea O&G industry continues its decline but it is counteracted by slow growth in the offshore wind sector. However, despite the slow growth, offshore wind has also been hit by inflation with profitability eroded and project risks remaining high. There remain some optimistic signs including recent project consents and the potential of floating wind. This means OSV demand could continue to hinge on offshore wind activity in the region.

It should be noted that Europe is a major driver in environmental regulations and operator appetite for cleaner OSVs. The EU is leading regulatory emission reporting through EU-MRV, and the EU ETS (which will impact around 18% of the OSV fleet when it’s introduced to the offshore fleet in 2027). As such, this is boosting the uptake in enviro-friendly upgrades such as ESS, alternative fuels and other emission-reduction technologies. In turn there is a strong correlation between these technologies and higher utilization rates.

Brazil’s Petrobras is the main driver of OSV activity in South America. Yet, with Petrobras reducing its offshore investment, will decreased activity from the state operator result in a shift to stabilization over growth? We foresee continued growth, but the drivers will be IOC deepwater programs both in Brazil and elsewhere in the region: Guyana is already accounting for high OSV demand and Suriname is well placed as an up-and-comer.

Like Europe, the region has regulations which result in a direct impact on the fleet. Brazilian regulations have imposed rules requiring vessels to be Brazilian-flagged and crewed. This has created a real challenge for the country to attract new players as they will be obliged to re-flag and develop a strong in-country presence. So, to encourage fleet renewal, Petrobras has diversified its approach by asking for increased numbers of newbuilds to have long-term charters.

Like South America, APAC will find much of its demand from a state-owned operator: Petronas in Malaysia. With O&G production ramping up, demand for floater rigs is booming—up to seven rigs are expected to enter the region from late 2025. Elsewhere, demand is rising in Australia driven by the Ichtys and Gorgon project extensions.

For more in-depth analysis on the future of the OSV fleet watch the replay of our recent webinar: ‘OSV Market Outlook: Identifying the next growth drivers’.