Hugo Madeline

,

Senior Offshore Energy Analyst / Project Manager

Author

, Published on

March 23, 2026

No items found.

Analysis of the subsea vessel fleet including its resurgence of interest and expectations for the future.

The multipurpose subsea vessel market is set to see a wave of deliveries in the coming years. In this insight we examine the resurgence of interest in this vessel category along with analysis of the current fleet and a look to the future.

Multipurpose subsea crane vessels — with crane capacities ranging from 50t to 400t — are versatile assets designed for subsea operations, including the installation, inspection, maintenance, and repair of underwater infrastructure.

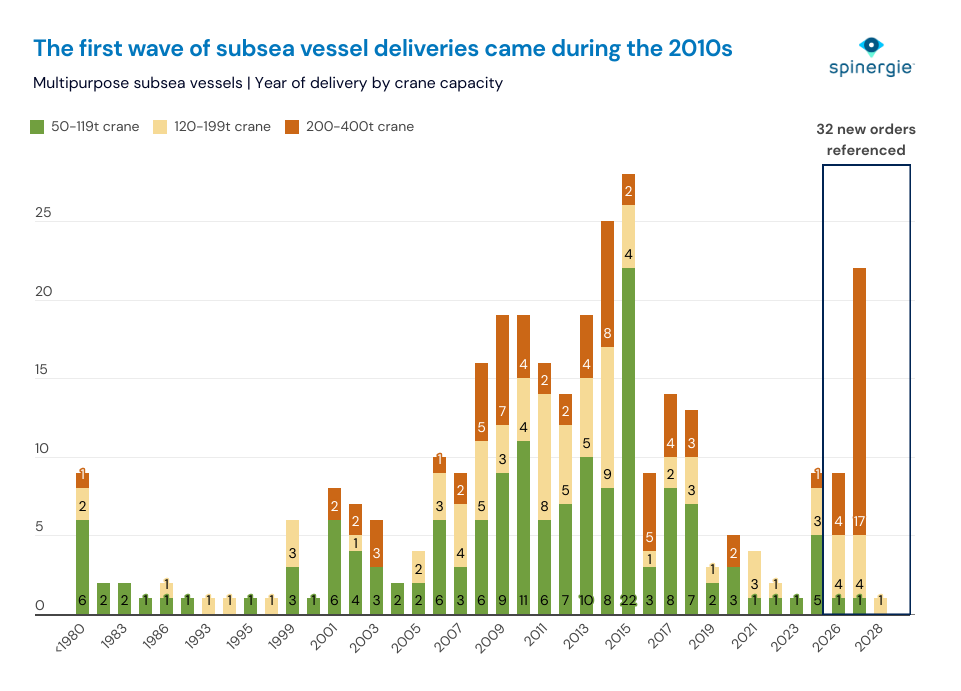

The first major wave of new builds occurred around 2010. This wave was driven by high levels of oil and gas (O&G) activity and vessels were purpose-built to support these offshore energy developments. This 2010 peak marked a shift in fleet composition—medium and large crane vessels gained market share ahead of the light crane vessels which had previously been the norm.

Today, the average fleet age is around 16 years old. Several owners are initiating renewal programs due to anticipated sustained market demand and long-term activity.

The main categories of multipurpose subsea vessels:

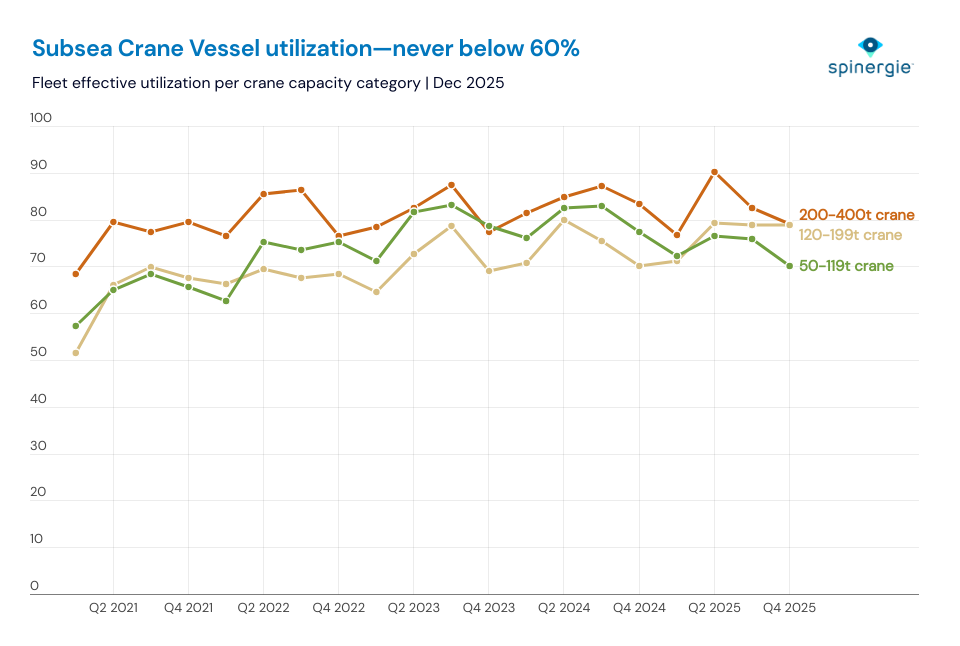

The MPSV and subsea vessel fleet experienced a swift recovery following the COVID-19 downturn, with utilization levels exceeding 70% across all segments by 2022.

The large crane vessel segment (200t and above) consistently achieved the highest utilization rates, remaining above 80% throughout the period—an indicator of steady demand for high-capacity subsea assets.

This combination of strong utilization, an aging fleet, and continued momentum in offshore developments (particularly in subsea construction and maintenance) has encouraged owners to place newbuild orders.

Despite some recent market softening, the long-term outlook remains positive, with fleet renewal driven by both technical obsolescence and anticipated project activity.

Some owners, such as SEA1, are introducing high-spec vessels designed for dual-purpose deployment across both subsea and offshore wind markets. This design flexibility reflects a broader trend toward multi-segment adaptability.

To address evolving industry needs, several owners now market their vessels as “Energy Subsea Vessels”, positioning them as versatile assets capable of operating in both O&G and renewable energy projects. This approach allows operators to remain flexible and opportunistic in securing contracts across sectors.

A similar dynamic is already visible in the CSOV market, where some players are leveraging light crane vessels to capture O&G opportunities. Conversely, subsea crane vessels could increasingly seize construction opportunities in the offshore wind sector, particularly as installation activity grows.

Looking ahead, a “U-shaped” fleet renewal pattern is expected. Assuming vessels are replaced after 30 years of service, the market may see a short-term decline in deliveries, followed by strong growth, potentially peaking at over 20 new units by 2040. Finally, long-term tender activity could reinforce this trend.

Competing demands from the oil and gas industry and a growing offshore wind sector has led to operators rethinking their fleet strategies. In our upcoming webinar we’ll be sharing how to choose the right mix of vessels and helicopters for efficient, safe, and cost-effective light O&M. Find out more here.