Maélig Gaborieau

,

Senior Offshore Wind Analyst

Author

, Published on

March 23, 2026

Yvan Gelbart

,

Lead Analyst

Co-Author

Larger offshore wind projects bring both unique installation challenges and the innovative technologies used to solve them. As monopiles grow in size, the use of pile grippers increases. Spinergie’s lead analyst Yvan Gelbart, and senior offshore wind analyst Maëlig Gaborieau, explore the pile gripper market in this blog post.

.jpg)

As offshore wind projects increase in size and scope, the challenges surrounding installation increase. This means that the sector must also turn to innovative technologies that support these larger projects and component sizes.

One of the key technologies used to enable the installation of larger monopiles is pile grippers, specifically motion-compensated pile grippers, which are used on board heavy-lift installation vessels.

Note: The analysis presented in this blog post focuses on the heavy-lift fleet outside of China. It includes legacy pile-guiding tools and gripper-arm arrangements, which assist alignment but do not provide the same level of control, sensing or active compensation.

A pile gripper is a deck-mounted frame or ring used during offshore wind construction to hold and steer a monopile while the hammer drives it into the seabed.

In modern heavy-lift installation vessels, these systems are hydraulically actuated, clamp the pile securely, and monitor its inclination and heading in real time.

When fitted with motion compensation, they actively stabilize the pile against wave-induced movement, helping operators maintain tight verticality tolerances.

As technology develops, monopiles have grown heavier and wider. As they now exceed 10 metres in diameter, traditional guiding tools and legacy gripper-arm systems no longer provide sufficient control.

Motion-compensated pile grippers address this by offering higher precision and allowing installation operations to continue in more challenging sea states. However, they are far from standardized. Each unit must be engineered to match specific vessel requirements, including maximum pile weight, diameter, and length. This level of customization means pile grippers are typically tied to specific vessels or campaigns with unique needs.

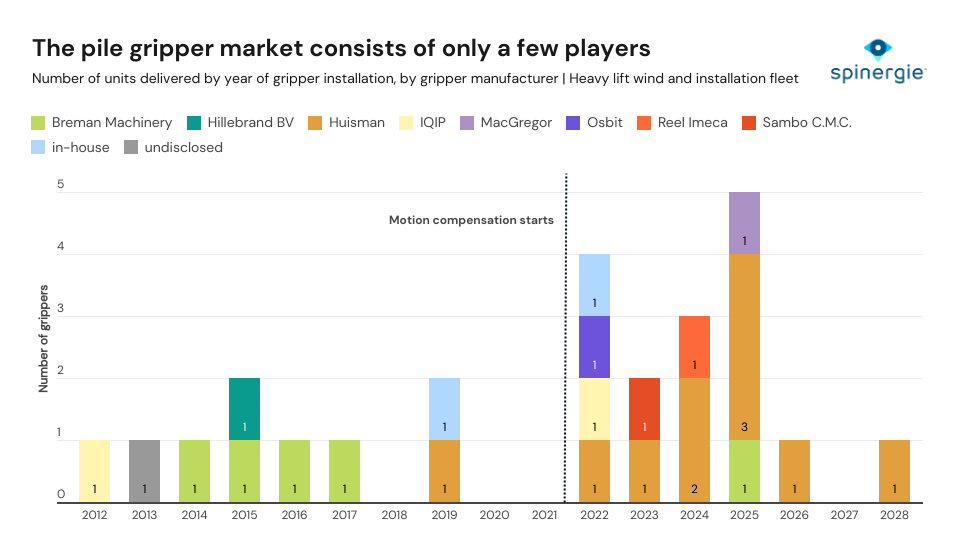

The supply landscape spans integrated designer-fabricators, pure manufacturers, and engineering firms that design but outsource production. Here, “manufacturer” refers to the first two categories, responsible for final delivery.

With eight delivered units, and two expected in 2026 and 2028 respectively, Huisman dominates the global pile gripper market—by far the largest share of the existing fleet. Breman Machinery ranks next with five units, primarily through its role as a subcontracted fabricator for TWD-designed grippers.

Beyond these two major suppliers, the market comprises in-house builds and a handful of small manufacturers, each responsible for only one or two deliveries. Overall, supply is moderately concentrated at the top, followed by a long tail of fragmented, low-volume contributors.

Edit on February 2, 2026: market sources indicate that the MacGregor pile gripper (2025) was cancelled before delivery.

Early offshore wind vessels typically entered service with simple pile guiding tools or gripper-arm arrangements, and no motion-compensated systems were present in those initial generations.

Deliveries slowed sharply between 2018 and 2021, but activity rebounded from 2022 onward, with newbuild programs driving a steady pace of three to five units per year. These recent models increasingly incorporate motion compensation, a milestone first achieved in 2022 with the gripper built for DEME’s Orion, a TWD/DEME design fabricated by Huisman. Since then, inflation and broader macro-economic pressures have curbed investment, leaving only two firm deliveries expected for 2026–2028 (Wind Ace and Penta Ocean HX118).

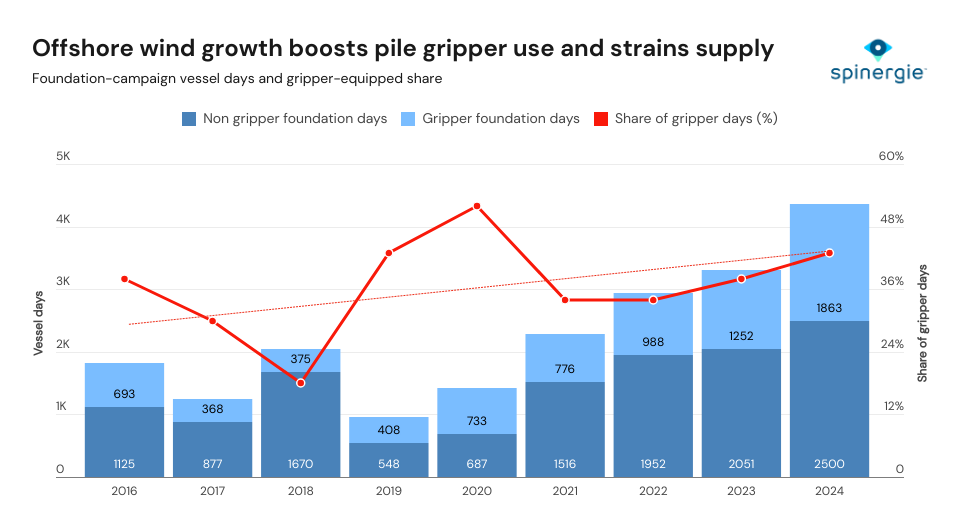

Pile gripper use has trended upwards amid offshore wind expansion.

Foundation-campaign activity more than doubled between 2016 and 2024. Throughout this period, the share of vessel days completed with gripper-equipped units fluctuated within a 20–50% band and averaged around 40%.

Despite year-to-year volatility, adoption displays an upward trajectory as larger monopiles and tighter installation tolerances increasingly favor vessels fitted with modern grippers. Overall, the rise in gripper-equipped days broadly tracks with the underlying growth in offshore wind demand.

Spinergie’s outlook points to a clear capacity gap: five to 10 pile grippers could be missing at the 2029–2030 demand peak, even before considering high-adoption scenarios.

Interested in learning more about Spinergie’s coverage of offshore installation equipment, from grippers to heavy-lift systems? If you are exploring market dynamics, or planning for upcoming investments, we can support you with dedicated equipment-focused analyses. Find out more by scheduling a free, personalized demo.

Feature image—Jan De Nul via: Jan De Nul to install foundations for large offshore wind project in Scotland (27 Feb, 2025)