Hugo Madeline

,

Senior Offshore Energy Analyst / Project Manager

Author

, Published on

March 23, 2026

No items found.

South America’s OSV market shows structural resilience despite a softer 2026 market. Here we share an analysis of the main market drivers in this key region.

South America’s offshore vessel market remains one of the most structurally resilient globally. Despite moderate fleet additions, utilisation across AHTS and PSV segments continues to hold steady. This blog post outlines the drivers behind this consistently high utilisation and suggests that, while the market may be softer in the near term, it is built for overall stability.

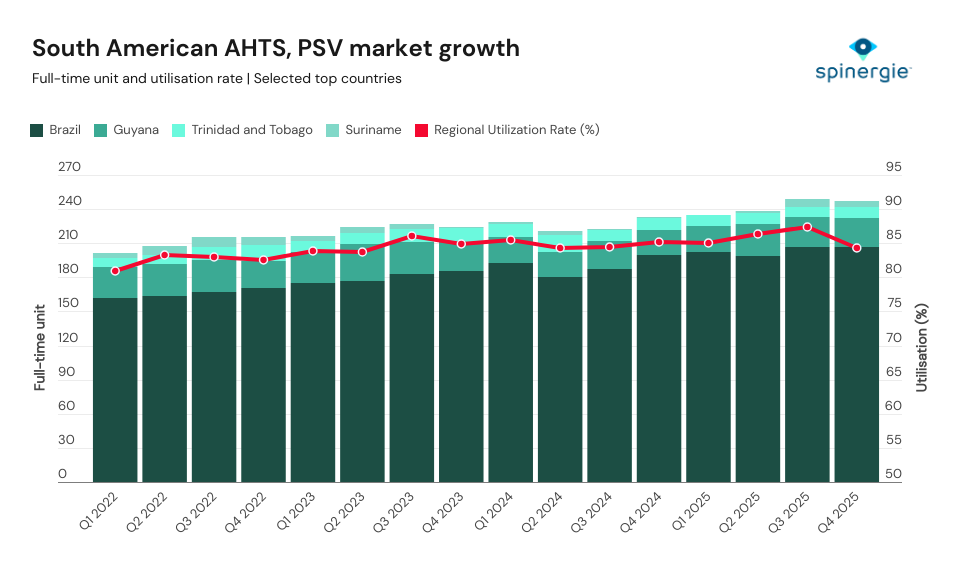

The South American AHTS and PSV market has recently been categorised by steady fleet expansion and consistently high utilisation. This has demonstrated the structural strength of offshore activity in the region.

Growth has primarily been driven by Brazil’s FPSO-centric development model. This, alongside the ramping up of activity offshore Guyana, has created sustained demand for both PSV and AHTS.

Despite moderate fleet additions, utilisation has remained resilient around the low-to-mid-80% range, indicating there is currently limited oversupply. This confirms that current demand is operationally, rather than speculatively, driven. Vessels are largely absorbed by long-term FPSO support, drilling campaigns, and production logistics.

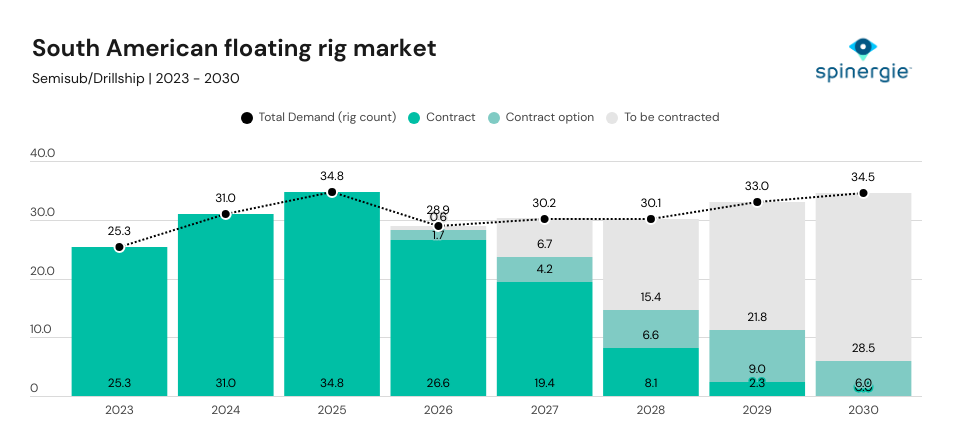

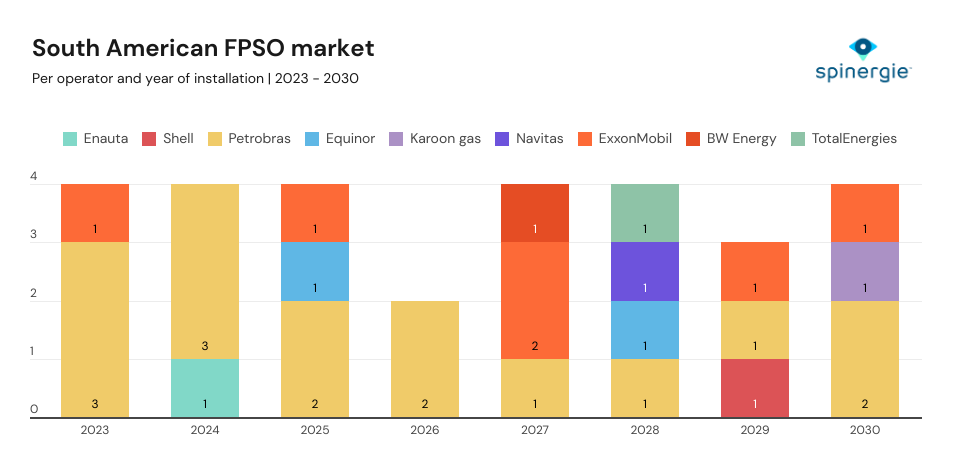

The most active deepwater drilling market in South America, Brazil, is expected to soften throughout 2026. This follows reduced investments and a shift to focusing on operational execution by state operator Petrobras. In its 2026 - 2030 Business Plan, Petrobras outlined how it would refocus on strategic projects and aim at reducing operating expenses to 8.5%—down from 12% in the 2025 plan. As such, the company will prioritise cost control and project execution, including nine FPSOs.

While Petrobras' near-term decline may be partially mitigated by contract extensions for locally owned drilling units, overall demand is forecast to remain largely flat through 2026–2028 as several projects are deferred or reverted to earlier phases. Despite Petrobras’ planned reductions, it is expected to maintain its leadership in the Brazilian market. At the same time, IOCs' activity is projected to grow, accounting for an average of 22% of regional activity.

South American FPSO demand is expected to enter a temporary soft patch from 2026 driven by fewer project sanctions in 2023–2024 and Petrobras’ emphasis on cost control and execution of a limited set of core projects. This is likely to cap utilisation rather than trigger a sharp decline, as fleet growth remains controlled and local operators benefit from contract extensions.

From 2028–2029 onward, utilisation is expected to recover gradually as postponed FPSO projects and deferred developments re-enter execution. The outlook supports a flattening–then-recovery profile, rather than a structural downturn, for AHTS and PSV demand in South America.

The key takeaway is clear: South America’s offshore demand remains fundamentally supported by long-term production infrastructure, not short-cycle speculation.

To see how global and regional market dynamics impact vessel utilisation, fleet supply, and demand in real time, book a demo of Spinergie Market Intelligence. Our solution helps you make faster, data-driven decisions for your offshore projects.