Hugo Madeline

,

Senior Offshore Energy Analyst / Project Manager

Author

, Published on

March 23, 2026

No items found.

The SOV/CSOV fleet is growing rapidly but faces short-term oversupply from offshore wind delays, prompting owners to diversify their strategies. Senior offshore energy analyst Hugo Madeline shares the state of the market in this update.

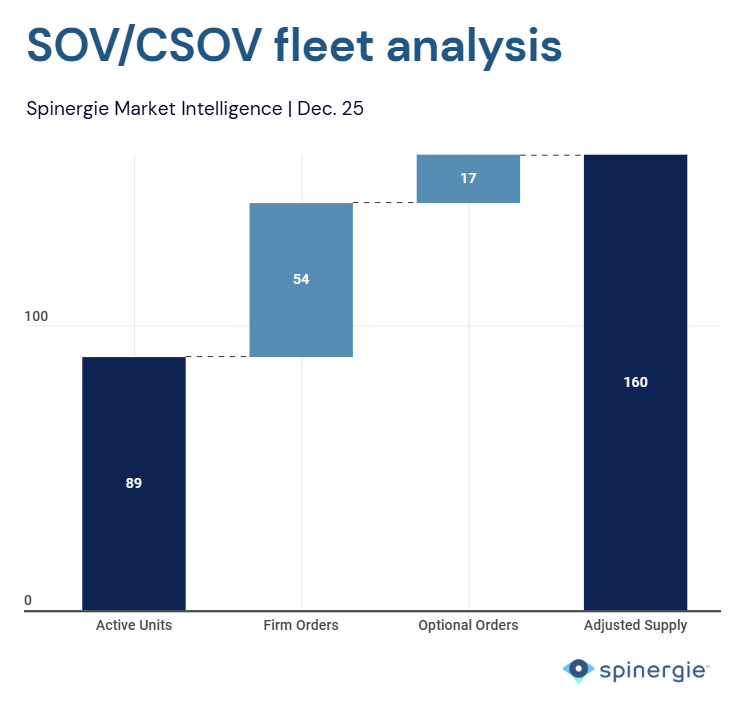

Service Operation Vessels (SOVs) and Commissioning Service Operation Vessels (CSOVs), bridge the gap between crew transfer vessels and subsea units, rapidly making them essential assets in offshore wind logistics. The fleet has seen unprecedented expansion, with 16 units delivered in 2024 and up to 25 expected by the end of 2025, marking the fastest growth among offshore segments.

This acceleration stems from highly favorable market and financing conditions observed between 2022 and 2023, when vessel owners placed multiple newbuild orders, buoyed by ambitious offshore wind targets and accessible capital. Many of these contracts were underpinned by long-term charters with wind developers or OEMs, ensuring financial security at the time.

Today, utilization remains high, often between 80% and 100%, for the contracted fleet, illustrating the strength of the market. However, the macroeconomic environment is shifting rapidly: rising interest rates, inflationary pressures, and project postponements are reshaping the balance of supply and demand across the sector.

The SOV/CSOV segment is still emerging, filling a gap in construction support and operations & maintenance (O&M). CSOVs, in particular, were developed to compete with larger vessels traditionally used in the oil and gas (O&G) industry for turbine completion, array cable pull-in, and commissioning tasks.

With an average construction lead time of two years, the current wave of deliveries reflects investment decisions made during a bullish period for offshore wind. Two main ordering strategies emerged:

Vessels built on speculation are now exposed to spot market volatility. With 47 projects canceled in 2025, the slowdown in wind investment has created an oversupply risk in the short term.

An illustrative example is the Olympic Notos, which, after serving through offshore wind projects, recently secured a five-year charter with AkerBP for operations in the Yggdrasil area — albeit it requires a retrofit. This deal highlights a growing trend: cross-sector redeployment, as owners increasingly shift toward O&G contracts to manage offshore wind uncertainties. The current market bifurcation came from the investment strategies adopted in 2022.

North Star Group demonstrates a conservative, contract-focused approach, with 10 firm units, all supported by long-term (10–15 -year) offshore wind charters. Their additional two optional units are likely to proceed only once similar contract security is secured — emphasizing the company’s controlled management of capital.

By contrast, Norwind adopted a speculative approach by ordering units without firm employment commitments at delivery. While initially risky, this strategy has proven flexible. The company has successfully redeployed some vessels into the O&G spot and term markets, including a recent bid for the Norwind Storm in Brazil.

These contrasting strategies show that flexibility and diversification are becoming key strategic priorities in an increasingly cyclical and interconnected energy vessel market.

The blurring boundaries between offshore wind and O&G support operations are driving the next evolution of vessel design. Developers and operators alike prefer hybrid, multi-purpose vessels—which have recently secured the new name “Energy Subsea Vessels”—that can operate efficiently across both markets.

Recent examples reinforce this pivot:

This new generation of vessels is part of a strategic response to market uncertainty, allowing owners to switch between sectors based on project timing and investment flows.

The fleet's long-term outlook remains promising. Nearly 200 SOV/CSOV units are expected by 2030, with a significant share set to work in the Asia-Pacific region. Dong Fang illustrates the APAC market dynamic with three units ordered. Yet, the aggressive expansion phase gives way to a more selective and strategic period.

While offshore wind remains the structural driver for SOV/CSOV demand, the short-term landscape is characterized by slower project sanctioning, tighter financing, and rising competition. In this environment, owners are under pressure to lock in contracts early and, where possible, diversify into adjacent markets. Speculative tonnage faces the greatest exposure, reinforcing the need for cross-sector flexibility.

The rise of “energy vessels” captures this turning point: the industry is moving to a pragmatic fleet optimization.

This year has been a correction phase, not a contraction. Continued growth in offshore wind will reinforce the vessels’ core market, while a steady pickup in O&G activity could stabilize utilization and provide alternative employment.

Operational decisions in offshore wind are becoming increasingly complex. Wind farms are moving into deeper waters farther from shore, turbine sizes and counts are increasing and fleets are evolving. This raises a major question: how do operators navigate between CTV, SOV, and Helicopters to keep light O&M operations efficient, safe, and cost-effective? Our upcoming webinar will use real-time data and forecasting to help you plan and strategize for your O&M scopes. Find out more here.