Sarah McLean

,

Lead Content Manager

Author

, Published on

March 23, 2026

No items found.

The recent failure of the German offshore wind auction for North Sea sites N-10.1 and N-10.2 has once again highlighted the issues surrounding negative bidding. But what can revitalize confidence in future auctions?

.webp)

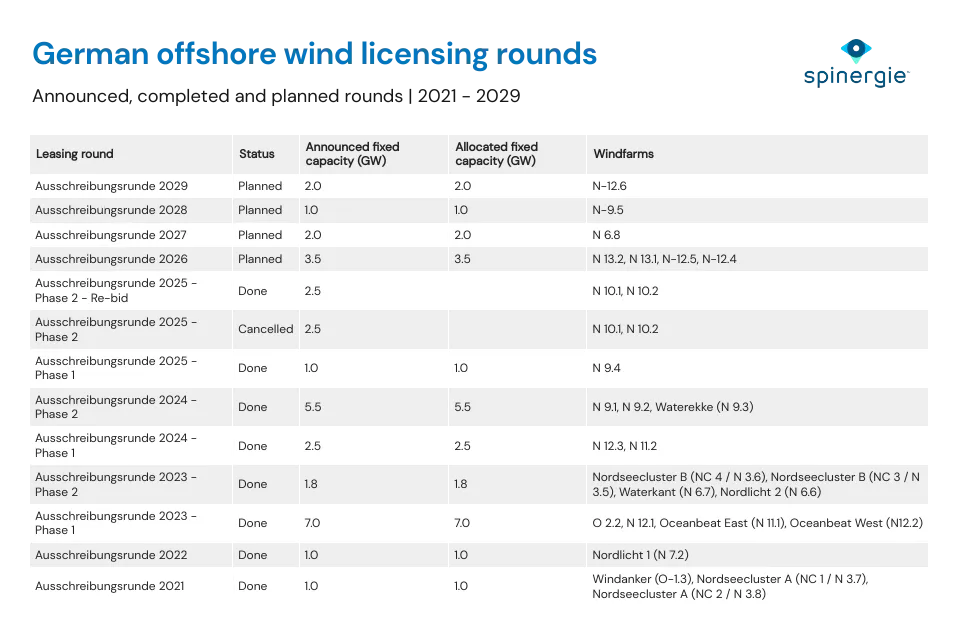

In early August it was confirmed that the second German offshore wind auction of 2025 had failed with not a single bid placed. Two sites had been offered in the German North Sea—N-10.1 and N-10.2—with a total capacity of 2.5 GW.

While there were a selection of issues with this particular wind auction, including technical challenges, the negative bidding nature of the auction was the key problem—one which continues to raise its head.

The negative bidding auction model has been controversial since the first such auction in mid-2023. In a negative bidding auction developers must bid the money they are willing to spend for the right to build a wind farm. This has several downsides. As in the first German negative bidding auction in 2023, it means that those with more cash are those more likely to win. In the Ausschreibungsrunde 2023 - Round 1 auction, two traditional oil and gas companies were the winners, with offshore wind developers expressing fears that the costs involved would ultimately be detrimental to the offshore wind sector.

Negative bidding auctions ultimately increase costs for developers and these costs must be passed on somewhere down the line whether to the supply chain, which is already under pressure, or to customers. While they provide a short-term revenue for the host Government, they create long-term risks that developers cannot take in the current climate and provide an unattractive prospect for investors.

Following the most recent German auction failure, Stefan Thimm, Managing Director of the German Offshore Wind Energy Association, said: “The fact that not a single company participated in this auction is a foregone conclusion. The industry has been warning for years against burdening companies with too many risks. However, the legal requirements no longer take into account the framework for investments in offshore wind projects in Germany. The current auction design forces developers to bear risks beyond their control without any protection.”

It has been reported that the same sites will be offered for tender once again by Germany’s Federal Network Agency.

The recent German auction is not alone in its failure to attract bids. In December 2024, a Danish auction round (for 3 GW total capacity) also ended without any bids. Like the German auction, there were additional circumstances that contributed to its failure. Denmark does not pay for the grid connection to offshore wind farms resulting in an additional cost to developers.

Further complications arose from “the fact that Denmark’s electricity demand from mobility, heating, hydrogen producers and industry is not picking up fast enough. Denmark is already frequently covering its electricity demand to 100% from renewables today. For offshore wind developers this creates uncertainty around the price they can sell their electricity at in the future,” as stated by WindEurope.

The follow up to this auction failure was a suspension of all ongoing offshore wind tenders in Denmark, with the acknowledgement that the no-subsidy model wasn’t working under current market conditions.

While the design of these negative bidding auction rounds is the main factor behind their failure, is the answer the more traditional Contract for Difference (CfD) model? In a CfD auction round governments issue a tender in order to procure a certain capacity of wind-generated electricity. In CfD auctions developers submit their bids with a strike price per unit of electricity at which they are able to realise the project. Bids are then evaluated on the basis of price, alongside other criteria such as innovation, before a power purchase agreement is signed.

The key difference in revenue between the two structures is that with a win in a negative bidding auction will result in a revenue being the wholesale market price of electricity. Meanwhile, for a CfD auction, the revenue is whatever you bid. Should the market prices be higher than the agreed strike price then the difference is paid to the government. This means that the upfront costs involved in a negative bidding round are not there in a CfD auction.

Yet, CfD auctions must also be handled properly and have seen their own share of failures. In September 2023, the UK announced that there has been a single bid for its 5th Contract for Difference (CfD) auction with WindEurope deeming the round “badly-designed.” In this case, the UK Government had set a maximum strike price of £44/MWh, including the cost of grid connection. This was far too low for developers to build a cost effective project, especially in light of recent inflation.

The lack of bids in negative bidding rounds suggests that the offshore wind sector is starting to push back against governments. Indeed, earlier this year the Dutch government was forced to rethink a tender process for two offshore wind sites after a lack of interest. Developers Eneco and Orsted stated that they saw no business case for the sites without subsidies. As such, the Netherlands will now only open one 1 GW North Sea location for tender.

Offshore wind developers face countless challenges in today’s market from reduced revenue certainty, to pressures to meet capacity goals under unrealistic timelines to a lack of wind infrastructure in certain markets to a supply chain under pressure. Therefore, whatever the auction structure, it is clear that they must be designed to fit the needs of the sector, with clear guidelines and rules, and make sense economically. As seen in the UK’s CfD Round 5, auction prices must reflect the actual costs of wind farm development, otherwise they will be an expensive disaster for all parties.

Governments have begun to take note. Denmark is taking steps to revitalize interest in its acreage following the failure of 2024’s auction. A new round, with capacities up to 6 GW across various sites, is expected this autumn (2025) and leaves negative bidding behind to follow the CfD state subsidy model with additional features more attractive to developers. The framework allows for more timeline freedom with flexibility in installation year and relaxed penalties for delays. It also outlines state-funded site investigations and surveys while also removing mandatory state ownership in wind projects.

This new framework for the upcoming Danish round shows more trust in developers, while providing the support needed to ensure projects can proceed successfully. It is hoped that it will have significantly more bids than the 2024 auction failure as the three projects have the potential to more than double the country’s current offshore wind capacity.

In uncertain times, as much visibility and certainty as possible is fundamental—this is what a CfD auction offers, even more so when the strike price is adjusted for inflation. Furthermore, offshore wind auctions, and the Governments that hold them, need to inspire confidence in the developers who will be bidding for the acreage, not raise uncertainty and questions. To do so, collaboration is key.

Wind developers have been vocal in their criticism of auction design, but Governments can learn from these criticisms and work together with the developers to create frameworks that work for everyone. Otherwise, the ambitious capacity targets outlined globally will have no chance of coming to fruition.

For more information on how Spinergie can help you track upcoming offshore wind leasing rounds and navigate the supply chain contact us for a demo today.