Hugo Madeline

,

Senior Offshore Energy Analyst / Project Manager

Author

, Published on

March 23, 2026

Maélig Gaborieau

,

Senior Offshore Wind Analyst

Co-Author

As SOV use increases in both the wind and O&G sectors, Spinergie analysts Hugo Madeline and Maëlig Gaborieau examine whether this growing fleet will cope with demand.

.webp)

The following is adapted from a longer article originally published in Maritime Journal. You can access it here

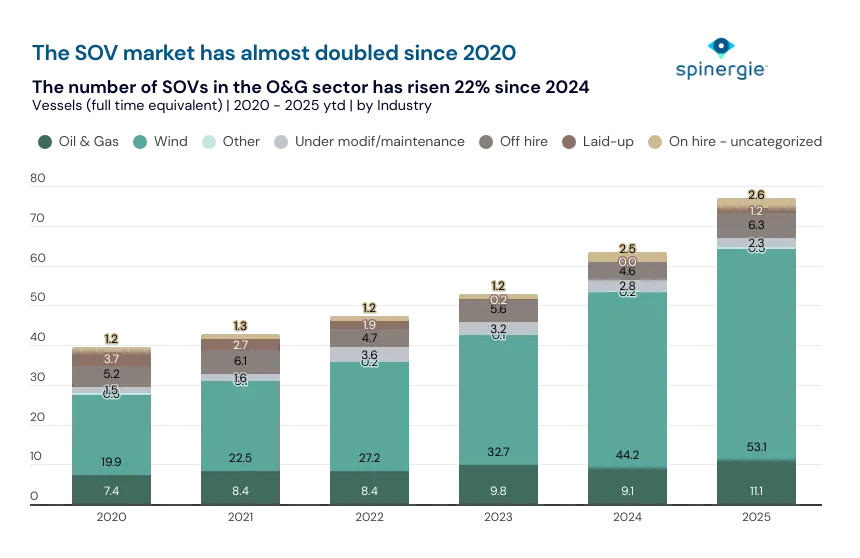

The Service Operation Vessel (SOV) market is going through a period of rapid expansion driven by two main factors: a growing demand for wind-specific offshore support and more commercial opportunities in the traditional offshore energy market.

Purpose-built for the wind market they play a major part in maximizing offshore working time with greater endurance and longer operating windows than crew transfer vessels (CTVs). Unlike CTVs, which return to port daily, SOVs can remain at sea for up to 15 days, farther offshore and in harsher conditions. They have a dual role, working in construction, where they take on the acronym CSOV, and in operations and maintenance (O&M).

Yet oil and gas deployments are also rising and are up 8% year-on-year since 2019, signaling an evolution in the commercial scope of these vessels.

In the construction phase, SOVs support a number of operations:

In the foundation completion phase, CSOVs support final inspections, bolting, welding, and protective coating to prepare foundations for turbine installation.

In turbine commissioning, CSOVs assist with testing mechanical, electrical, and control systems. This includes functional checks, system calibration, and initial energization.

Each construction phase involves light crane operations to move tools, equipment, test devices, and spare parts to the turbine. These tasks were traditionally handled by medium multipurpose or construction vessels, but Spinergie analysis shows that CSOVs are now replacing many of these assets and gaining market share.

As offshore wind projects move into deeper waters, the use of SOVs increases due to their operational abilities and crew capacities. This is in comparison to CTVs, which are more suited for near-shore projects.

SOV activities in O&M include planned interventions such as scheduled turbine maintenance, inspections, and minor repairs. They can also be used in reactive operations such as unplanned light maintenance following component failure or sensor alerts.

With onboard workshops, spare parts storage, and motion-compensated gangways, SOVs enable technicians to address issues promptly without the need to return to port, maximizing turbine availability and reducing logistical delays.

As of August 2025, the global SOV fleet includes 85 active vessels with another 48 expected to be delivered over the next few years—32 of which in 2025 alone. In addition to the expected reach of 133 vessels in total, there are a number of assets currently under option.

A drop in SOV demand is anticipated around 2027, due to expectations that a lack of heavy-lift vessel availability will cause bottlenecks in the offshore wind project pipeline. In response to this, vessel owners are adapting their strategies. A common strategy is to lock in tri-partite agreements—binding contracts between the vessel owner, ship designer, and offshore wind developer—for terms of five to 10 years. The fleet itself continues to evolve with a number of mid-sized SOVs entering the market to bridge the gap between CTVs and full-scale SOVs.

In the near term, the SOV market is set to remain supply-constrained rather than demand-limited. Fleet expansion is moving fast, but with utilization already exceeding 80%, and with cross-sector competition from oil and gas, vessel availability will be the key pressure point. As owners lock in long-term agreements and adapt vessel designs, the next phase of the market will be defined less by whether demand exists, and more by how quickly purpose-built SOV capacity can keep pace.

Find out more about our comprehensive CTV, SOV and CSOV report here. The report includes a detailed analysis of SOV/CSOV and CTV demand in the offshore wind sector through 2040 with additional coverage of market trends, growth forecasts and vessel dynamics at national, regional and global levels. The study also includes detailed supply analysis covering the current fleet, upcoming newbuilds and long-term fleet evolution