Maélig Gaborieau

,

Senior Offshore Wind Analyst

Author

, Published on

March 23, 2026

No items found.

Mapping the global rebound in offshore wind FIDs, with an exploration of how easing macro conditions and strategic financing are driving new CAPEX momentum across Europe and APAC in 2026.

.jpg)

Final Investment Decisions (FID) in offshore wind are a solid indicator of momentum within a given region. In 2025, Northern Europe showed strong momentum with a marked increase in CAPEX commitments compared to 2024 levels. Yet, on the other hand, North America was frozen by regulatory headwinds and APAC had a similarly quiet year, albeit one which shows promise for this year and beyond.

In this outlook, senior offshore wind analyst Maëlig Gaborieau shares the key projects that reached FID in 2025 including historic moves in Poland. It also maps the strongest candidates for investment decisions for the remainder of 2026.

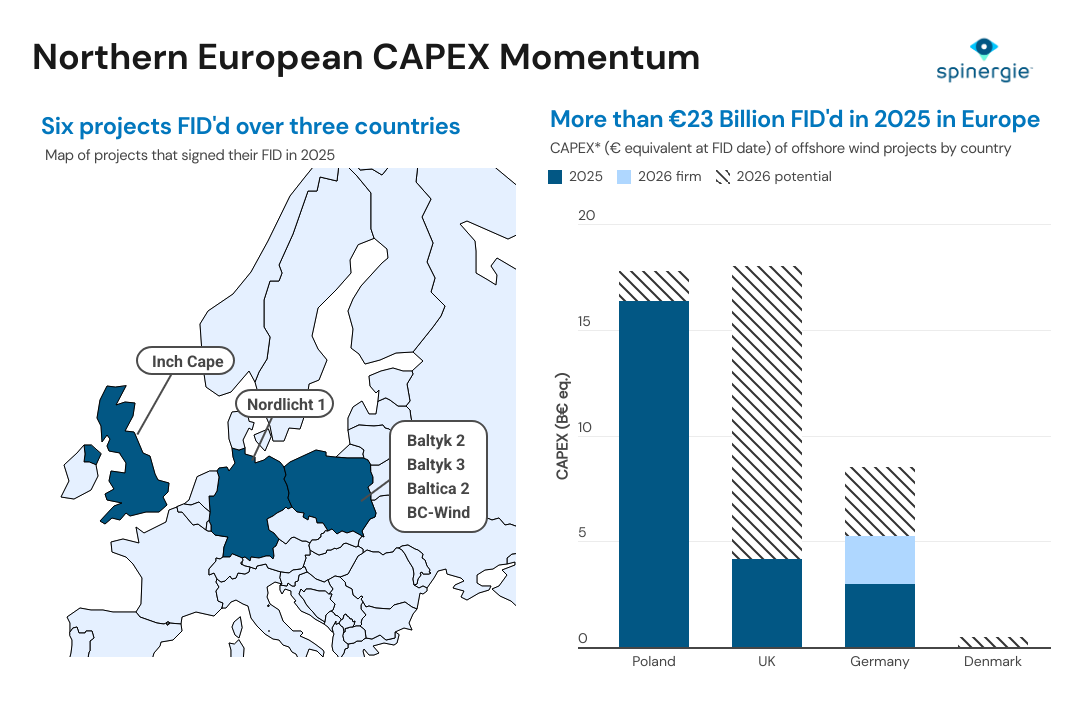

Northern European FID activity rebounded in 2025, with projects reaching that stage representing over €23bn of CAPEX. While this number was up from the €9bn recorded in 2024, it still fell short of the record €28bn reached in 2023.

Significant contributions came from the UK and Germany. In the UK, Inch Cape reached FID just four months after securing capacity in Allocation Round 6. With construction of the project already underway, Inch Cape is a key example of strong developer confidence and advanced project maturity. Meanwhile, Germany contributed with Vattenfall’s Nordlicht 1 achieving FID, ahead of Nordlicht 2 in early 2026.

The most significant shift occurred in Poland, however, where Baltyk 2, Baltyk 3, Baltica 2 and BC-Wind all progressed to FID in the same year. Together, these projects represent more than €12bn of CAPEX. These projects reflect the rapid scale-up of the Polish offshore wind industry, which is supported by solid policy frameworks, expanding infrastructure and a maturing local supply chain.

Looking ahead to the remainder of 2026, Northern Europe remains the core region for potential offshore wind FIDs, with the UK again leading the pipeline. RWE’s Norfolk Boreas and Norfolk Vanguard are the most advanced candidates, having secured CfDs in Allocation Rounds 4 and 7, providing strong revenue visibility ahead of investment decisions.

In Germany, Gennaker is also well advanced, with key contracts signed and its final permit granted in December.

Denmark appears as a new entrant compared with 2025, with TotalEnergies’ Lillebælt Syd project adding limited but tangible capacity. At 165 MW, its modest size reduces execution risk and increases the likelihood of reaching FID in the near term.

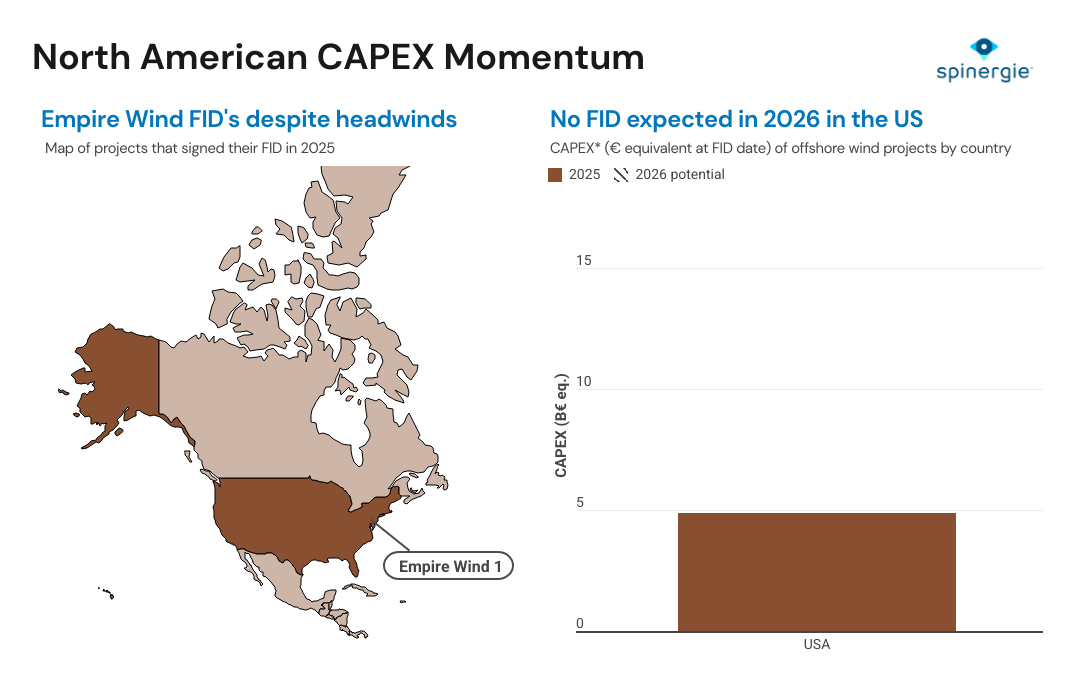

Offshore wind FID activity in North America remained extremely limited in 2025. In fact, only one project - Equinor’s Empire Wind 1 - reached that stage shortly before the inauguration of President Donald Trump in January.

Since then, the policy environment for offshore wind has deteriorated significantly, creating persistent uncertainty for developers. On 16 April, the Department of the Interior instructed BOEM to immediately halt all construction activities on Empire Wind pending a federal review. Although work resumed one month later, the project was again paused in December 2025 before restarting in January 2026.

This sequence of interruptions highlights the fragility of offshore wind development under the current administration. Given the openly hostile stance toward the sector, and the resulting regulatory volatility, the likelihood of investments and additional projects reaching FID during this presidential term (expected to run until 2029) appears impossible.

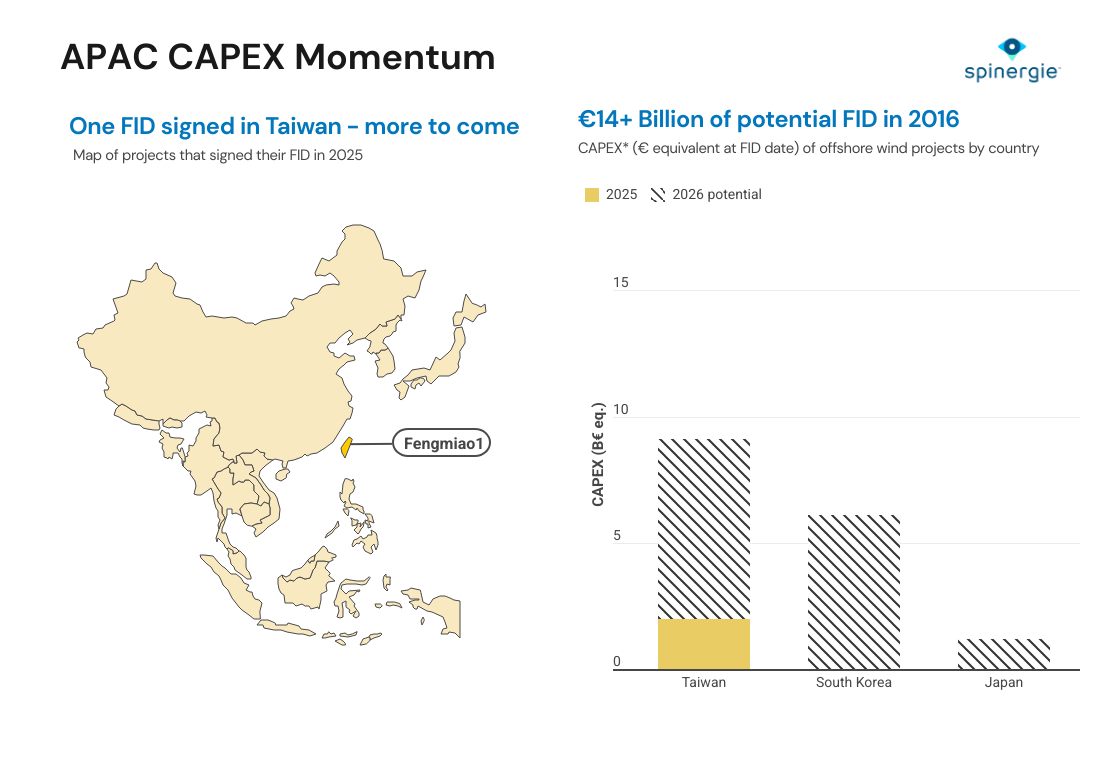

The APAC region (excluding China) also only saw one offshore wind project reaching FID in 2025. This was despite multiple developments continuing to progress toward investment readiness. Fengmiao 1 in Taiwan achieved FID in March, developed by Copenhagen Infrastructure Partners securing a portfolio of long-term power purchase agreements with a diversified group of corporate offtakers, including Google, MediaTek, and United Microelectronics Corporation (UMC). This strong corporate demand played a central role in de-risking the project and enabling investment in an APAC market reliant on private offtake structures.

Looking ahead to the remainder of 2026, APAC offshore wind FID activity is expected to increase and broaden geographically.

In Taiwan, Formosa 4, developed by Synera Renewables, stands out as a leading candidate, with key installation and supply contracts already secured, significantly de-risking the path to investment decision.

Japan could also emerge as a newcomer compared with 2025, as ongoing reforms to the permitting framework improve project bankability. In this context, JERA Nex BP’s Oga City, Katagami City and Akita City project, a relatively small-scale development with 21 turbines, could reach FID in 2026.

South Korea is also advancing, with Hanwha’s Shinan Ui project making steady progress and approaching investment readiness. In addition, Vena Energy’s Taean project strengthened its commercial foundation in 2025 by signing multiple corporate power purchase agreements totalling 500 MW, improving project economics and increasing the likelihood of an FID in the coming year.

The offshore wind outlook is increasingly shaped by macroeconomic conditions rather than purely industrial constraints. The easing of interest rates and inflation throughout 2025 has materially improved project economics, creating a more supportive environment for both developers and suppliers to commit capital in 2026. Sustained periods of lower financing costs are particularly critical, as a 1% increase in the cost of financing can translate into an estimated 8–12% increase in Levelized Cost of Energy (LCOE), making financial conditions a decisive driver of FID activity.

While past bottlenecks were largely concentrated around installation vessel availability and supply chain constraints, the industry has progressively shifted toward a financing-led challenge. In response, developers are increasingly structuring projects through joint ventures with investment funds, allowing risk sharing, balance-sheet optimisation and reduced upfront capital exposure, ultimately facilitating the pathway to FID. That is why 2026 is a promising year for FIDs.